I once wrote a blog post about a public figure that got a lot of attention. Some readers praised it, but one line in the post caused a major problem. A lawyer sent me a letter, claiming I had said something false. I was shocked—and scared. I had no idea that writing one sentence could lead to legal trouble. That’s when I first realized how important media insurance is.

You might face the same risks if you create or share any kind of content—whether it’s a blog, podcast, video, or ad. Having protection is preferable to being unprepared.

What Is Media Insurance?

Media insurance protects people and companies that create content. It covers you if someone claims your content damaged their reputation, broke copyright laws, or shared their private information without permission.

Writers, podcasters, influencers, filmmakers, marketers, PR firms, and even social media managers can benefit from media liability insurance.

Why Is Media Insurance Important?

In today’s world, content spreads fast—and mistakes can cost a lot. If someone believes your blog, video, or social media post harmed them, they can sue you.

For example:

- People who claim shows like Baby Reindeer and The Queen’s Gambit inaccurately depicted their real-life stories have filed multiple lawsuits against Netflix.

- In the UK, a company called Trinity Mirror had to pay millions due to claims about phone hacking and bad reporting.

- A small YouTube creator faced legal action for using unowned background music. That mistake could’ve been covered by media insurance.

Furthermore, with AI and deepfakes becoming more common, it’s now easier to accidentally post content that breaks laws or invades someone’s privacy—even without meaning to. If your content causes harm, someone might hold you responsible. That’s where media insurance steps in.

Who Should Get Media Insurance?

If you’re in any of these fields, you should seriously consider media insurance:

- Bloggers & Writers: If you publish online articles, reviews, or commentary.

- Social Media Managers & Influencers: If you run accounts or share content with followers.

- Video Creators & Podcasters: If you make entertainment, news, or educational content.

- Marketing & PR Professionals: If you create ads, press releases, or brand stories.

- Photographers & Designers: If your work appears in public campaigns.

Media insurance can shield you from unforeseen legal issues if the public publishes or views your work.

What Does Media Insurance Cover?

Media insurance usually covers:

- Defamation (libel or slander): Saying something false that damages someone’s reputation.

- Copyright Infringement: Using someone else’s content (like images, music, or writing) without permission.

- Privacy Violations: Sharing private info without consent.

- Plagiarism: Copying someone’s work and claiming it’s yours.

- Misuse of a Person’s Image or Name: Using someone’s photo or name in a way they didn’t agree to.

Not all policies cover the same things, so it’s important to talk to an insurance expert who understands.

Real-Life Examples

Here are some real situations where media insurance could’ve helped (or did):

- A social media manager posted about a competitor’s brand, and it turned into a legal problem. Media insurance covered the costs.

- A small business used a song in an ad without permission. The owner had to pay a fine. If they had media insurance, it might’ve covered the legal fees.

- A documentary filmmaker was sued after a person claimed they were wrongly portrayed. Media insurance helped cover the defense.

Even big companies make mistakes. If they can face legal action, so can we.

How Much Does Media Insurance Cost?

The cost depends on a few things:

- What kind of content you create

- How many people see it

- How often you publish

- The size of your business

A freelance blogger may receive a lower salary compared to a video production company. On average, media insurance can cost anywhere from $500 to $2,500 per year, depending on the risk level.

However, the cost of not having insurance could be significantly higher. Legal fees alone can go into the tens of thousands—even if you did nothing wrong.

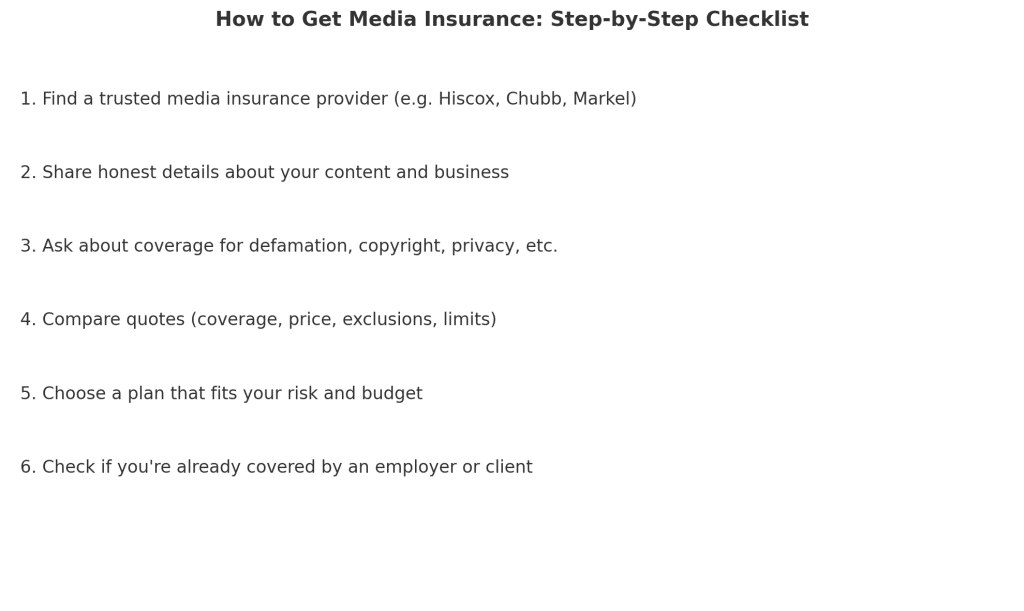

How Do I Get Media Insurance?

Getting media insurance isn’t hard, but you need to do it right. Here’s a detailed guide based on what I’ve learned from personal experience and expert advice.

#1. Find a trusted insurance provider that offers media liability insurance

Not every insurance company understands the unique risks of content creators, marketers, or media professionals. So, go for insurers that specialize in media, tech, and creative work.

Here are some top providers to consider:

- Hiscox – Great for freelancers, bloggers, and consultants. They offer quick online quotes.

- Chubb – One of the largest insurers in the world, with strong media-specific policies.

- AXIS Insurance – Known for insuring media companies and entertainment businesses.

- Markel – Offers flexible media liability and professional coverage.

- Vouch – Built specifically for startups and creators; fast digital process.

- The Hartford – Ideal for small businesses that produce content.

Tip: If you’re outside the U.S., look into local brokers who offer professional indemnity or media E&O coverage.

#2. Share details about your business and the kind of content you create

Be honest and clear when filling out forms or talking to an agent. They need to know:

- What type of content you produce (writing, video, ads, designs, etc.)

- Where it’s published (online, TV, newsletters, podcasts, etc.)

- How big your audience is

- Whether you work with clients or agencies

- If you use AI tools, stock content, or third-party contributors

Their knowledge helps them recommend the right policy—and it protects you from claim denials later on.

#3. Ask about specific coverage options and exclusions

Don’t just assume you’re protected. Ask direct questions like

- “Does this policy cover defamation lawsuits?”

- “What happens if I accidentally use copyrighted material?”

- “Will this cover privacy claims or social media mistakes?”

- “What are the policy limits?”

- “Does it include AI-generated content or guest content from others?”

Furthermore, check for exclusions—things they don’t cover. For example, some policies won’t protect you if you knowingly post something false or if your content is deemed to cause “intentional harm.”

#4. Compare multiple quotes before buying

Please obtain quotes from at least 2–3 providers. Look beyond the price—also compare:

- What’s covered vs. what’s not

- Maximum payout per claim

- Deductibles (how much you pay out of pocket before insurance kicks in)

- Customer service and ease of filing claims

- Whether the policy renews automatically and how changes are handled

Occasionally, the cheapest policy isn’t the best. You want reliable protection, not just a bargain.

#5. Choose a plan that fits your content risk and your budget

If you’re just starting as a freelancer or content creator, a basic plan for $500–$800/year may be enough.

If you run a team or agency or have a large audience, you’ll likely need a more advanced plan with higher limits. These limits can range from $1,000 to $2,500/year.

Good news: Most policies allow you to upgrade later as your brand or business grows.

#6. Check if you’re already covered under someone else’s policy

Before you buy:

- Ask your employer if their business insurance covers media risks.

- If you work with clients, please inquire whether they expect you to carry coverage or if they already have it.

- If you’re a member of a publishing team or creative agency, find out if their umbrella policy covers you.

You would rather not pay twice—or worse, find out too late that you weren’t covered at all.

What’s the Difference Between Media Insurance and General Liability Insurance

At first, both general liability insurance and media insurance might sound like they offer the same protection—but they cover two entirely different types of risk.

Let me break it down.

General Liability Insurance: Physical World Protection

General liability insurance protects your business against physical harm that happens because of your business activities.

It covers:

- A client slipping and falling at your office or studio

- Accidental damage to a client’s property during a shoot or meeting

- Legal costs if someone gets hurt or files a personal injury claim

For example:

If a client comes into your workspace, trips over your tripod, and breaks their leg, general liability insurance helps pay their medical bills and protects you from getting sued.

This type of insurance is usually required for renting office space, applying for business licenses, or getting certain jobs—especially in physical locations.

Media Insurance: Content Risk Protection

Media insurance, on the other hand, protects you against non-physical risks—specifically, problems that come from the content you create or share.

It covers things like

- Defamation (e.g., someone claims your blog or video harmed their reputation)

- Copyright Infringement (e.g., you used a photo or sound you didn’t have rights to)

- Invasion of Privacy (e.g., you used someone’s photo or story without permission)

- Plagiarism and Misuse of a person’s name or likeness

Why You Might Need Both

If you’re running a creative business—especially one that works in person and publishes content—you likely need both types of insurance:

| Scenario | What Covers You |

|---|---|

| Client slips in your studio | ✅ General Liability Insurance |

| Someone sues you for what you said in your podcast | ✅ Media Insurance |

| You damage a venue’s property while filming | ✅ General Liability Insurance |

| A company claims your design copied their logo | ✅ Media Insurance |

In One Line

General liability = physical injuries and property damage

Media insurance = content-related legal mistakes

Both are valuable, but they cover different sides of your creative work.

Does a Freelancer or Content Creator Really Need Media Insurance?

Yes—100%.

A large agency or production company does not necessarily face legal action. Even freelancers can get in trouble if:

- You write something a reader claims is false

- You post a photo without checking the license

- A client says your campaign hurt their brand

If you’re a content creator, blogger, or social media manager, media insurance is your safety net.

Is Media Insurance the Same as Errors and Omissions (E&O) Insurance?

Not quite. E&O insurance is for professionals (like lawyers or consultants) who give advice or services.

Media insurance is a type of E&O made specifically for creators and communicators. It covers risks like defamation, copyright issues, and more.

What Are the Risks of Not Having Media Insurance?

If someone sues you and you don’t have this insurance, you’ll have to pay out-of-pocket for:

- Lawyers

- Settlements

- Court fees

- Lost contracts or income

Even if you win, the costs of defending yourself can drain your savings or shut your business down.

How Can I Choose the Best Media Insurance Policy?

Here’s what I look for:

✅ Ask if they cover defamation, copyright, and privacy

✅ Make sure online content is included (social media, blogs, etc.)

✅ Check if AI content is covered

✅ Choose a company that understands media

✅ Read the exclusions carefully

Trusted providers include Hiscox, Chubb, Vouch, and Markel.

What Industries Need Media Insurance the Most?

You need media insurance if you work in:

- Blogging & journalism

- PR or advertising

- Podcasting or YouTube

- Social media marketing

- Education or coaching (with online content)

- Tech or SaaS (with user-generated content)

If your work goes public, you need coverage.

Will Media Insurance Cover AI-Generated Content or Deepfakes?

It depends on your policy.

Some insurance companies are starting to offer coverage for AI content and deepfake risks, like

- False advertising

- Copyright claims from AI-generated images

- Defamation from fake videos

If you utilize AI tools, please inform your insurance provider in advance and ensure that this type of risk is covered in your policy.

What Should Be Included in a Good Media Insurance Policy?

A strong media insurance policy should cover:

- Defamation (libel and slander)

- Copyright and trademark infringement

- Privacy violations

- Plagiarism

- Misuse of someone’s name, voice, or image

- Online content (social media, video, blogs)

- Legal defense costs

- International content use

How Do I File a Claim With Media Insurance?

It’s usually pretty simple:

- Notify your insurance company right away

- Share the details and any documents you have

- Let them handle the legal part

- Don’t admit fault—your insurer will guide you

- Keep records of all communication

A trustworthy insurance company will walk you through the whole process.

Can Media Insurance Protect Me If I Get Sued Over a Podcast or YouTube Video?

Yes—and that’s one of the most common uses.

If it’s a podcast or video,

- Says something that offends someone

- Uses music, images, or clips without permission

- Talks about a company or person in a way they find false

Media insurance can cover your legal defense and any settlement costs.

Key Takeaways

- Media insurance protects you from legal claims related to your content.

- Writers, creators, influencers, and marketers can all benefit from it.

- It covers things like defamation, copyright infringement, and privacy issues.

- Without insurance, legal troubles can cost thousands—even if you didn’t mean harm.

- It’s affordable, and it brings peace of mind when creating content.

Conclusion

Whether you’re running a blog, making videos, or managing social media, media insurance isn’t just “nice to have”—it’s essential. We all want to create freely without fear. But in today’s world, one small mistake can turn into a big legal mess. I experienced this firsthand, but you don’t have to.

So, what kind of content do you create—and are you protected against the risks that come with it?

Related Articles

- Crisis Management Insurance Coverage: How It Works

- Professional Insurance for Consultants: Why It’s Essential for Your Business

- MEDIA ANALYSIS: How To Conduct An Effective Media Analysis

- BROADCAST MEDIA: Meaning, Types and Examples